an informative guide to increase net worth

a collaborative effort with my favorite finance instagram accounts

Last August, I reached out to a few of my favorite finance accounts on Instagram and asked whether they were willing to contribute to an Instagram post about increasing net worth. Months later, after creating this Substack, I realized I wanted to not only make a graphic about it, but also create a “get-to-know-you” type post, where you get to learn more about how some of the contributors of this net worth post have gotten to where they are currently at now. For the Instagram post that pairs with this newsletter, find it here, where you can see each contributor’s current net worth.

Before we get started, let’s clarify how I’m conceptualizing net worth in this post. Net worth is value of the assets a person or corporation owns, minus the liabilities. However, how assets and liabilities are defined can differ for each person. I’ve made sure to standardize this in the Instagram post and this newsletter. Assets are restricted to liquid cash and investments (stocks, bonds, etc.). I have asked each person to exclude physical assets that some may use to calculate as part of their net worth (i.e., home, luxury bags, jewelry, car).

Without further ado, let’s dive into these questions.

talk about anything. your favorite things, movies, film, finance strategies, where you're from, etc. i’m hoping this will give my readers a good introduction as to who you are!!!

brainchildmoney — Hey, I'm Wren! Raised and rooted in the Midwest, USA. Health is a huge priority and I love yoga, camping, hiking, strength training, running, and cooking healthy food. Software Engineering is my current flavor of the week, but I'm a serial career pivoter intrigued with entrepreneurship. Being a connector of people and ideas is a core part of my identity. I'm on a solid upward trajectory with my money, so now I'm shifting focus to meaning, purpose, and building a life that's "enough".

ritual_finance — I’m Bree, a high school math teacher living in the Bay Area, California. During the pandemic I spent a lot of time learning about all things finance & that’s when I really started budgeting & investing more seriously. Most recently I’ve been working on finding the balance between truly enjoying my life now, while also responsibly preparing for the future. Some random facts: I’m a vegetarian, plant mom, aspiring minimalist who enjoys exploring new places (near or far!).

myfirebook — I'm 29, SINK living in a HCOL city in Canada. I have a passion for personal finance and currently working towards FI/RE. I spend my down time hanging out with friends, trying new fitness classes and watching reality TV (Love is Blind, Singles Inferno). Sometimes, I get bursts of motivation and watch entrepreneurship videos on Youtube.

centsofindependence — I am from Singapore and I quit my 9-5 job after making 1M. Now I am freelancing as a part-time tutor while sailing with my boyfriend. My life goals are to sail the world with my boyfriend, learn design/illustration and hopefully become a designer one day.

tessa_finance — Hi, everyone! My name is Tessa and I am a 25 year-old teacher living in the Canadian Arctic. My parents immigrated to Canada due to the Vietnam War and this led to me growing up in a low-income household. When I turned 22, I told myself that I had enough of living pay cheque to pay cheque and wanted to learn how the rich got rich. This fuel for financial independence led me to hustle for wealth and my biggest financial goal at the moment is to achieve my first $1,000,000. I hope to help many other people like me who came from nothing but will build an empire someday.

themoneyloaf — I'm just a regular loaf who has been in a corporate job for the last 15 years. I graduated right in the middle of the 2008/2009 recession and realised that relying on a job or saving is just not gonna cut it if I ever want to retire early - so I started finding ways to invest towards my freedom.

koreangalonfire — I'm a second gen Korean American living on the East Coast. I spent my 20s working at startups and in graduate school. After getting laid off in 2022, I spent a year traveling in Asia and learning how to trade. I'm also a licensed real estate agent and my goal is purchase my first property this year! My hobbies include yoga, pottery, volunteer on nonprofit boards, and making kimchi.

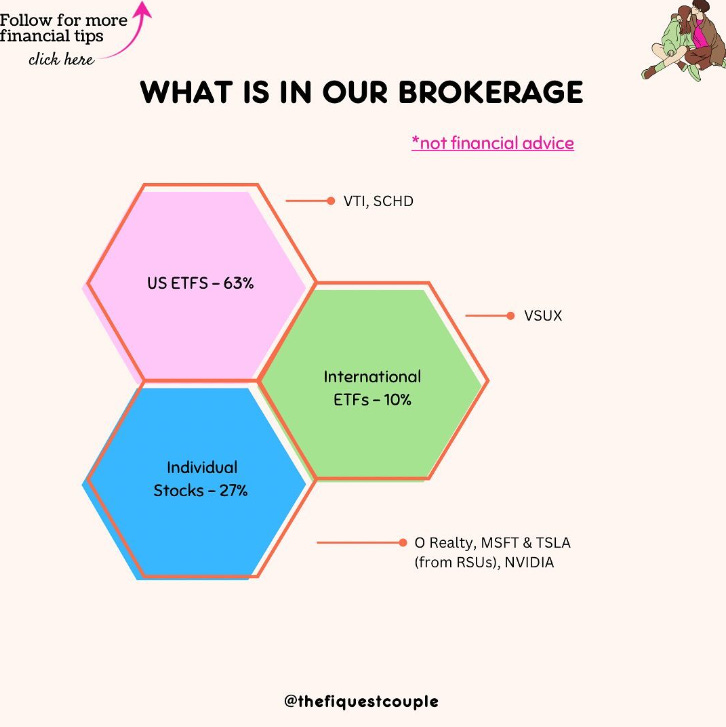

thefiquestcouple — My friends call me J and my family calls me by my middle name so that sometimes trip people when they hear the other name. I am a Kenyan immigrant in the US, and I met my husband on our first day of college and we have been together for almost 10 years! I am currently not working and just going to take the year off to do whatever I feel like. My favorite place I have visited were Ireland (scenery, people), Bolivia (landscape) and London (Incredible vegan food). We are both finance nerds - we created an investment thesis in 2022 that is our north star when it comes with building our financial future. Current goal is to be fully financially free by 2028 where both my husband and I do not have to work at all.

riseandshinemoney — Hi! I am an acupuncturist living on the west coast of Canada. I discovered a passion for personal finance when I began my journey to pay off 30k of student loans in under three years. I love walking in the forest, karaoke, making jokes, gold jewelry, spending time with friends and hanging out with the Bernese mountain dog at work. I also enjoy thrifting, reading, yoga and am interested in all things spirituality, self-inquiry and personal development.

softgirlfinance — Hi everyone, I’m SoftGirlFinance! I’m an INFP who values a life led by softness, slowness, and intentionality. I view money, and my pursuit of FI/RE, as a tool and source of freedom. Some of my interests and passions include self-development, fine dining, true crime podcasts, books that make me cry, options trading, playing volleyball, mental health, and spending time with my loved ones.

how did you increase your income, what field are you in, what is your current salary, etc.

brainchildmoney — I am a HUGE advocate of negotiation, upskilling, and networking as a means to increase income and opportunities. I negotiated early and often (gaining $44k+ in pay plus several other benefits like remote working agreements and Fridays off), gained new skills in high demand (learned how to code from scratch in my late 20s), and networked with people who could move my career forward (attended lots of events, meetup groups, and conducted informational interviews). Currently a Software Engineer, Fortune 500 Company, Salary: over six figures. In the $100-150k range

ritual_finance — As a teacher, I’ve been able to increase my income by taking online classes to earn more credits beyond my Master’s degree. We also tend to get pay increases with each new school year (some little, some big). Also- I was mindful about salaries when I applied to my first teaching job and was sure to choose a district that paid well. Current salary: $122,905

myfirebook — I work in data & finance. I've been in my role for 6 years. My current pay raise including bonus is projected to be $97,000 this year. Instead of job hopping, I asked my manager for a 20% pay raise two years ago and surprisingly, it was approved! I'm also in the process of completing certifications because I want to improve my technical skills.

centsofindependence — I have been in the education field for 20+years. I used to earn about $140k until I quit my full-time teaching job. Nowadays I earn $40-$60k per year depending on how many hours I teach.

tessa_finance — Alright, everything you need to know about my income! As a teacher, it is well-known that this is one of the most underpaid profession out there. For me to achieve my financial dreams, during my last year of university I researched different districts across Canada and the world that are offering teaching jobs. Seriously, I applied to Japan, United Kingdom, Sweden, Australia and tons more. By studying the collective agreements, I learned that the highest teaching salary were in Northern Canada and this is how I landed my first 6 digit job at 22 years old. Today, I am a 3rd year teacher making $117k. To continue to bump up my salary, I am also getting my master's degree (since my job pays $6k/year for professional development) and this will help me to move up the pay grid while working full-time.

themoneyloaf — I changed jobs a few times in my early years and negotiated hard for at least a 20% jump each time. I work in marketing and started at about $24k a year, now I make about $120k at my day job.

koreangalonfire — At my last startup job, my total comp was close to $300K including base, bonus, stock options, and benefits. My first startup job paid $60K. Over the years, I increased my income by negotiating raises and job hopping. Going to graduate school may or may not have helped. The number one creator of wealth for me was working at a unicorn startup that IPO'ed and became a multi-billon dollar company. As a newish trader, I'm hoping to bring in around $100K-$120K this year.

thefiquestcouple — When I graduated college, I got a job as a software engineer making ~$115k total comp. After my first year, I got promoted and my comp increased to $130k total. I was then laid off in 2023 and never went back to a corporate job. My husband and I have a couple of income streams outside of corporate which include 3 real estate properties and currently a business that we own. I spent most of last year freelancing as a part-time software engineer and did a lot of side hustles that include mystery shopping, focus groups and paid content creation. This year, I have yet to decide what I will be doing as I am not expecting a ton of work for pay. Our current non W-2 income is about $10,000/month and we expect that my husband will be getting $12,500 gross from the business before any profit sharing at the end of the year.

riseandshinemoney — As mentioned, I have worked in the alternative healthcare field for the past 7 years off and on. I have taken lots of steps over the years to increase my income, both in my acupuncture jobs and in other jobs I have worked along the way. This has included negotiating my contracts (I have a commission split for my main job), asking for merit-based raises, taking on more shifts, extending my hours, working overtime, working weekends, raising my rates when I was undercharging, etc. I feel happy with my current contract and appropriately compensated. I think increasing your income while still being mindful of your expenses is one of the best ways to pay off debt, increase your net worth and give yourself more buffer room between surviving and thriving. I haven't had extensive experience with negotiating salary, raises, etc but I know there are so many good resources out there for people in exactly this situation, especially if you work in corporate environments. Even though I share a lot on my IG page, I have decided to keep some details of my personal and financial life private, including salary. Let's just say that I have not yet hit making 60k per year but I hope to soon! My current net worth is 47k.

softgirlfinance — I’m a registered nurse, working in Canada. I’m going into my third year of nursing, and my hourly rate is ~$43 CAD/hr, not including shift premiums. These premiums are extra pay that nurses receive for working evenings/nights and weekends, holding a regular position, being in charge, coming in for a shift at the last minute (<24hrs), and etc. This amount can easily add up to an extra $10-15/hr depending on the shift. Since I’m part of a union, I have no control over my hourly rate and wage increases. As a workaround, I try to strategically pick up OT shifts when rates range from 2x-3.75x my base rate.

what was your experience w/ debt, what type of debt do/did you have, what methods did you use to pay it off?

brainchildmoney — I had student loan debt right after college and I paid it off very quickly by working 3 jobs. I had my regular office job (a resume builder) and took 2 additional bartending jobs.

ritual_finance — I was fortunate enough to have my tuition waived at any public CA university so for undergrad I went to UCSD. I only had to take out loans to pay for room & board. Similarly, for grad school I got a full scholarship so I only had to pay for my housing & food. I still took out all of the loans available to me that I knew would be forgivable after 5 years of teaching and used some of those to pay off my undergrad loans. Now I’m debt free!

myfirebook — The only debt I had (other than my mortgage) was student loans - I graduated with $6k in student loans. Most of my tuition was paid off through internships. I lived with my parents until my debt was paid off and I had a good amount in savings (no shame in living with parents!)

centsofindependence — I have a mortgage to service now. My CPF retirement account is helping me service it now. But I am also earning the same amount in cash as I intend to refund my CPF one day. I don't have any other debts and never did.

tessa_finance — Oh boy, the fun "debt" conversation. Growing up in a low-income household, debt was a consistent reason why my parents fought every single week. This experience taught me that we should never have debt and money is a very "hush-hush" subject. My first big girl debt was when I started university and applied for student loans. I think my total student debt was around $40k and at 18 years old, I was OBSESSED with counting every dollar. I worked 2 part-time jobs (in restaurants packing food deliveries) throughout university and worked every single weekend for 5 years. There were weekends where I would work at one job from 10:30am-3:30pm and go to my next job at 4pm-9pm. This hustle helped me graduate practically debt-free and today I have $16k of student loans but I have not paid it off because it is interest-free. My finance journey has nothing to do with those "get rich quick" stories, in fact I build wealth through working hard and hustling in my 20s.

koreangalonfire — I never had credit card debt and was privileged to graduate from college without debt thanks to my parents. The only debt I have is graduate school student loans, expected to be paid off in less than five years.

thefiquestcouple — I fortunately did not have a lot of debt (so did my husband). I got a scholarship for college and husband's school was paid for by parents. I graduated with ~$7000 in student debt that I took to do a study abroad program that I paid quickly once I had a full-time job. I paid a set monthly amount and then used a big chunk of my first year bonus to pay off the rest.

riseandshinemoney — I have had one type of debt in my life and it was student loan debt! I accumulated 30.4k of student loan debt over the course of getting a university degree and and my acupuncture diploma. While this is a relatively average amount for student debt in Canada---and also a lot lower than much of the student debt I hear about in the US--it was an amount that felt like it was holding me back from living my life. Every time I got paid or wanted to spend, I felt like it wasn't really my money because I owed so much to the government. It felt like a huge weight on my shoulders when I thought about someday maybe having kids, buying a home, etc. So in January 2020 I went full force on my debt, planning to pay it off within one year. I was right on track to do that when COVID hit and threatened to derail my plan completely. However, I decided to shift the plan and focus on building up an emergency fund since the world was so unpredictable. I did that and when I had enough saved to feel comfortable / secure, I resumed my payments. I became debt free May 2022 and have since focused on saving and starting to invest.

My strategy: because I had only one type of debt, I didn't have to decide between the snowball or avalanche method. I just kept a bit of savings and through every dollar I could at my student loan. I divided my total debt amount by 12 months to figure out how much to pay each month. I stuck to those big payments until COVID hit when I paused as my loan had no mandatory payments and wasn't accumulating interest. I did everything I could to increase my income and focused a lot on decreasing my expenses and living very simply until my debt was paid off. I learned to budget, track my spending, sold old things I didn't need anymore, took on a part time job, journaled about money, set up visual reminders and checklists for my goals, increased my hours at work, told my friends what I was doing and stuck to my plan. I also worked in little rewards along to way to keep my motivated. It worked and the feeling of financial peace has been worth every effort.

softgirlfinance — My only experience with debt is student loan debt. Currently, my student loans are at 0% interest, so I’m paying the minimum payment every month. Personally, taking out student loans was a positive experience and the best thing I could have done for myself at the time, because it allowed me to also receive grants and bursaries, which covered the majority of my expenses while I was in post-secondary.

what investing strategies do you employ at this moment? what is your most profitable investing strategy? are you risk averse/tolerant/seeking? what is your advice to people who are new to investing? what is your advice to people who want to learn more about options trading or buying a property?

brainchildmoney — I am a relatively lazy investor. My investments include ETFs in a brokerage, maxing out my retirement accounts, investing my HSA, and Roth IRA. I would advise new investors to invest lazily, meaning ETFs; stuff that tracks the total stock market so you practically can't lose in the long run. DO NOT stock pick as your first entry into investing. ETFs can literally take you all the way to a fruitful retirement if you invest over a long term. The dollars you can invest per year have a limit, but the amount will be higher the more of them that are pre-tax (401k, HSA, etc.) vs investing post-tax dollars. I wanted to turbocharge things in my own life a bit, so I own rental property as well. Advice—Bigger Pockets books + Google is literally all I needed in terms of resources to get in the game, though support from my partner and a lunch with an experienced real estate investor helped push us in the right direction too.

ritual_finance — My only real investment strategy is to buy and hold. I invest in low cost index funds and take advantage of the tax advantaged accounts that are available to me (Roth IRA, 457b, & 403b). When I felt ready to start learning more beyond what I knew, I took @themoneyloaf options course and learned so much. I’m dabbling in that, but still need to spend more time going back through the course to really develop a deeper understanding. I highly recommend the course if you’re interested in how to make money through options. If you’re completely new to investing in general, I recommend reading a book. I loved “I Will Teach You To Be Rich” and “Quit Like A Millionaire”. They are packed with easy to understand info and are such an affordable way to learn!

myfirebook — I own one real estate property, and the rest of my NW is in stocks. I'm currently trying to have a consistent income trading options. My most profitable investing strategy is buying & holding real estate, and my investments in tech ETFs have also done really well. My advice for people new to investing is to be patient. There isn't a get rich quick scheme. Learn about the stock market, bond market, real estate market and other asset classes. Assess your risks. When it comes to investing in real estate, calculate your cash flows and vet your tenants carefully. Also make sure you know the landlord/tenant laws in your jurisdiction.

centsofindependence — I invest in broad-based ETFs like IWDA and SPY. Most of my capital is deployed there as I used to DCA $2k per month to IWDA when working full-time. I did invest some money in crypto (mainly btc and eth) and the investment paid off handsomely as crypto took off after 2020. I am still vested at this time. Other than that, most of my net worth is in my CPF retirement account and property with a small amount in REITs. Investing in index funds changed my life. I don't worry when the index plunges. In fact I buy more if I can. Investing in bitcoin has made me more accepting of risk. I started by investing $100 at a time. Then I increased the amount as I got more comfortable. I had my share of scams and rugpulls during these 3 years and lost a fair bit of money. But overall I am still net positive. Albeit, a more cautious investor. It’s super easy to start, but you must not be lazy.

Open a IBKR account

Transfer a comfortable amount every month. Automate this.

Automate the transactions in IBKR.

tessa_finance — I currently invest in natural diamond, gold, crypto currency, ETFs, some single stocks, and working on buying my first rental property. I am a huge believer in diversifying my investments and never putting everything into one basket. Since I am "young," I have a middle to high risk tolerant and in my mind, I have lots of time to fix any financial mistakes. At the moment, my most profitable investment is the stock market. I dumped about $100k into the stock market in 2021-2022 and have a profitable return of around $20k. For anyone new to investing, I would recommend to do your own investments because the fees advisors charge are just not worth it in the long run (imo). If you are interested in looking for cash flowing properties, I talk a lot about this on my Instagram but it is important that you find a really good real estate agent (especially when buying a property virtually like I am). My long-term goal is to build a big real estate portfolio and live all over the world hehe.

themoneyloaf — People might know me as an options trader, but I think I am one of the most risk averse options traders around! I don't like the idea of winning a few big trades and losing the rest, so I try to aim for a more sustainable strategy. Honestly I think the vast majority of people are better off buying index funds and holding them for 30 years. The difference is that I just hate being a corporate slave :D

koreangalonfire — I have 3 buckets of investments:

Retirement accounts: I only invest in ETFs. I didn't maximize my retirement accounts when I was in my early 20s and it's the one thing I wish I had done. In my last two jobs, I did max out my 401(k)s, which make up the bulk of my retirement investments

Short term trading: I actively trade options, as we well as day + swing trade with the goal of making a 5% return on capital monthly. While I am generally risk averse, I am more aggressive with these investments given the returns I seek.

Long term holdings: The majority of my investments are long term investments in a mix of ETFs, high-growth stocks, and dividend stocks. Tax implications of selling these are a major consideration.

I used to focus on dollar-cost averaging and holding investments all investments for as long as possible, but as I've become more active in managing my investments have changed my approach. I seek to capture profits when possible and of course protect my capital with active risk management.

thefiquestcouple — In 2023, our biggest investment was saving up for our business acquisition which we just closed on. Going forward, our biggest area of focus is to max out retirement accounts when we can (Roths, HSA, solo 401k, etc) and invest the rest of the money into long-term index funds in our taxable brokerage account. I will say that both my husband and I are very risk tolerant and taking asymmetrical bets is where we are right now. For newbies, I will say the easiest is to invest in retirement accounts either work provided such as 401ks or Roth IRAs and putting in a learning plan on what their risk tolerances are, what assets sounds interesting / easy to get into. There are a lot of resources on investing online but also spending some time with a professional can sometimes be a faster way to lower barriers to entry.

riseandshinemoney — I am extremely risk-averse financially! Investing has been a struggle for me emotionally so far. Money for me relates heavily to security, so investing has always felt a bit like gambling. It was key for me to set up an emergency fund for the peace of mind to know I have money saved if my investments drop. I have been slowly building up my tolerance to a fluctuating market but it's slow going. I started with one year GICs, then 2 year GICs. I have played around with a small amount of money in stocks just to get used to how the market changed. Another thing that holds me back a bit from investing is really caring a lot of about responsible and ethical investing. I don't want to be investing in things like military weapons and fossil fuels that perpetuate war or contribute to other harmful industries. I feel like there is a lot of cognitive dissonance between advocating for societal change / our beliefs in our real lives but then our finances literally being invested in those same harmful industries doing well. In the past year I have started banking with a credit union and they only offer socially responsible investing, so I look forward to learning more about it! I am still a baby when it comes to learning about investing but I love Ramit's advice about investing in target date index funds and ETFs, so if that's compatible with responsible investing then that's the avenue I would like to go. My advice to others would be to get yourself to a place where you have enough of a buffer of saved money that you start to feel comfortable investing. It's okay to dip your toes in at first and go at your own pace. Find someone you trust, put the time in to understand what you're investing in. Look at some online calculators that compare saving and investing so you can see how important it is to get to a place where you feel secure enough to invest. Look at compound interest calculators so you can see how staggering the difference is when you start ASAP to maximize time in the market. These lit a fire under my butt!

softgirlfinance — Currently, I am a fan of value and growth investing, and have recently started trading options. I buy and hold a small number of ETFs, and primarily hold individual stocks. I also trade options as a way to diversify my streams of income.

My most profitable investing strategy has been starting early and investing aggressively! The power of compound interest is life-changing. Since I'm young and have minimal responsibilities, I try to invest >50% of my income each month. My risk tolerance is quite high, but this is also because I'm investing for the long-term. As I get older, I will likely invest less of my income and move my money into less risky investments.

My advice to those who are new to investing is to just start. Start where you are and invest what you can. Investing is as simple, or as complicated, as one makes it. It can be as simple as buying a set dollar amount of a broad market ETF once every month, or be more complicated with researching individual stocks, options trading, and etc. The most important thing is to have your money working for you, in whatever way that aligns with your personal risk tolerance.

My advice to people who want to learn more about options trading is to be curious, cautious, and realistic. Personally, I only sell options, as a way to limit my risk. If you’re interested in learning on your own, reading books and watching videos is how most people start. If you’re interested in taking a course from someone, do your research! Look for unbiased reviews and read into the person who is teaching the course - do they have your best interests at heart? Or are they promising you a get-rich-quick scheme? Start small, be patient, and don’t overleverage yourself. Earning some money is better than losing a lot of money.

what were some lifestyle changes that you went through (or didn't) on your wealth building journey?

brainchildmoney — I've started living like a middle class college kid instead of like a poor college kid :) I was SUPER frugal in college and for the first few years after. I now spend about $10k per year more than I did just after college, which allows me to buy myself nicer foods to cook, go on a few international trips and handful of domestic trips per year, reward myself for money wins with experiences from my wish list, go to occasional concerts and events, buy nice gifts for important people in my life, and worry about money a bit less.

ritual_finance — I lived with my dad for about 4 years and during that time was able to save quite a bit of money. However, I also spent a lot of money on eating out, getting my hair done because I wasn’t paying much rent and didn’t feel stressed about money at all. When I finally moved out and started paying a shit ton of money in rent, I realized I had to be much more mindful about where I was spending my money and I cut back on a lot of things.

myfirebook — I've always been taught at a young age to save money and be super frugal, so that lifestyle hasn't changed throughout my wealth building journey. However I've been more focused on my health lately. As I've gotten older, I see the importance of maintaining a healthy lifestyle. I'm now more lenient to spend money when it comes to health (gym memberships, fitness classes, multivitamins, organic food, etc).

centsofindependence — 7 years ago, when I first started seriously tracking my expenses and investing my money, I also started reading this book called "The art of tidying up" by Marie Kondo. Her book taught me to say goodbye to everything in my life that does not spark joy. And that really changed my lifestyle and habits. Today I lead a minimalistic and free life because I focus only on things that sparked joy. I cut my hair really short. Almost everyday, I wear a uniform - my favorite Uniqlo airism blouse, Decathlon shorts and Havianas. In my backpack, I carry around my laptop, foldable phone and powerbank - which I use for almost all my needs i.e. work, social, entertainment, finance. I could literally live out of a 30L backpack if I wished to. So when I reached CoastFI in 2021 and quit my job, there was really not much adjustment to be done in terms of changing lifestyle or cutting expenses.

tessa_finance — Where do I even begin? LOL. Moving to the Arctic for a higher salary was a COMPLETE flip to my lifestyle as a city girl. First, I now live in a small town with no restaurants, no gym, no movie theatre, no swimming pool, and only 2 grocery stores. My biggest expense in the city was food deliveries and dining-out (I love girl's night lol), but living in the Arctic I had to learn to cook for 10 months of the year. Welcome world of meal prepping! I now live an extremely frugal and minimal lifestyle because buying anything "extra" in the Arctic will be a nightmare to move back to the South. Seriously, I wear the same 5 outfits every week to school. On the flip side, my 2 months every summer in the city is filled with "luxury" and I think wealth building requires a balance. My biggest fear is looking back in my 20s and regretting that I never enjoyed it to the fullest so every summer I travel, eat, and attend concerts to fill my soul. Summer 2023, I went to 16 concerts and 7 cities but still saved $65k cash by the end of the year. There is no right way to building wealth and everyone is in different situations but I hope we can all achieve our rich life, whatever that could look like. :)

themoneyloaf — So many! I've bounced from "I've earned this money, I deserve to spend it on something nice" to "If it doesn't hurt, I'm not investing enough". Currently I'm just trying to find a nice middle ground, but it's a work in progress.

koreangalonfire — Spending $40Kish on a year of travel and adventure was something I could never have imagined when I was in my early twenties. Having an emergency fund, savings, and a general financial cushion enabled me to continue spending even when I didn't have an income when initially laid off. I have continued to give (gifts and donations) and participate in intentional lifestyle inflation.

thefiquestcouple — At the beginning, we definitely were YOLO (husband and I met in college, so we started earning roughly around the same time). We did not budget and put our money towards lifestyle and experiences. We started seriously budgeting in 2023 and adopted a minimalistic lifestyle (materialwise) which has done wonders to our finances. Being aware of lifestyle creep and choosing what spending brings the most joy and meaning to us has also made us feel like we are living our rich lives without wasting money on things that don't matter.

riseandshinemoney — This started when I began paying off debt. I started tracking finances and budgeting for the first time in my life. I started eating almost exclusively at home (coffee shop visits, take out and restaurants REALLY add up). I did a lot more free activities with my friends. That usually ended up being going for long walks, which was great because this was during the early months of COVID so it was one of the only ways we could spend time together anyway. Having friends over for dinner and vice versa instead of going out. Really cooled it on the shopping. Not popping into thrift stores all the time and avoiding situations where I would impulse buy. I journaled a lot about money, about my goals and how I wanted to feel and what steps I could take to get there. I kept any local travel very inexpensive and tried to keep transportation costs down by walking or biking when possible instead of driving. I focused on buying good quality things secondhand. I drank less alcohol (especially out and about... it's so expensive!) I went through several relationship changes during this process, so I have adapted my finances and lifestyle whether I have had a live-in partner, long distance partner or been single. I kept an emergency fund for the first time in my life. I've also recognized the value of investing in myself, so I have enrolled in an amazing alternative therapy course that will help deepen my work, expand my toolkit and also allow me to offer a combination service at a higher hourly rate.

softgirlfinance — I’ve always been mindful of my spending, and have recently adopted a “value-based spending” mindset. I’ve learned that cutting costs on things I care less about, frees up room in my budget for things that I love. I'm living my life for me and pursuing FI/RE for me, and don't feel the need to impress or explain myself to anyone. For me, the biggest way I’ve cut down on my expenses is by living in an older apartment with cheap rent, and splitting rent with my partner. I also don’t own a car, nor have any particularly expensive hobbies, and I minimize my spending on clothes, takeout, subscriptions, and household items. This allows more room in my budget for fine dining, travel, volleyball drop-ins/clinics, getting my lashes done, and etc. Overall, I value living below my means and investing aggressively for my future, but I refuse to deprive myself of things that I find love and find joy in.

Thank you to the contributors of this post and on Instagram for all your valuable insight on increasing net worth.

Instagram, where I’m the most active and post stories every day about my life, every non-essential purchase I make, my Goodreads/Letterboxd reviews, my progress with my academic papers goal, and more!

I use Wealthfront for my high yield savings account, and if you use my link, we both get 0.50% added to their current APY for the first three months! The base APY at this moment is a whopping 5.00%.

All my Notion templates can be found and purchased here. Follower favorites are the Capsule Wardrobe Tracker and Digital Goal Setting Toolkit.

Here’s my Bento for all my links consolidated into one webpage!

See you next week,

damn this is much content I'm going to have to read it over days. thanks for the informative post.